apisadmin

About apisadmin

Posts by Sharon Elsberry:

September, 2017-Simple Charitable Life Insurance

Brad Gordon, President MAF Companies

MERP

The MERP strategy saves on average 20-30% of medical premiums

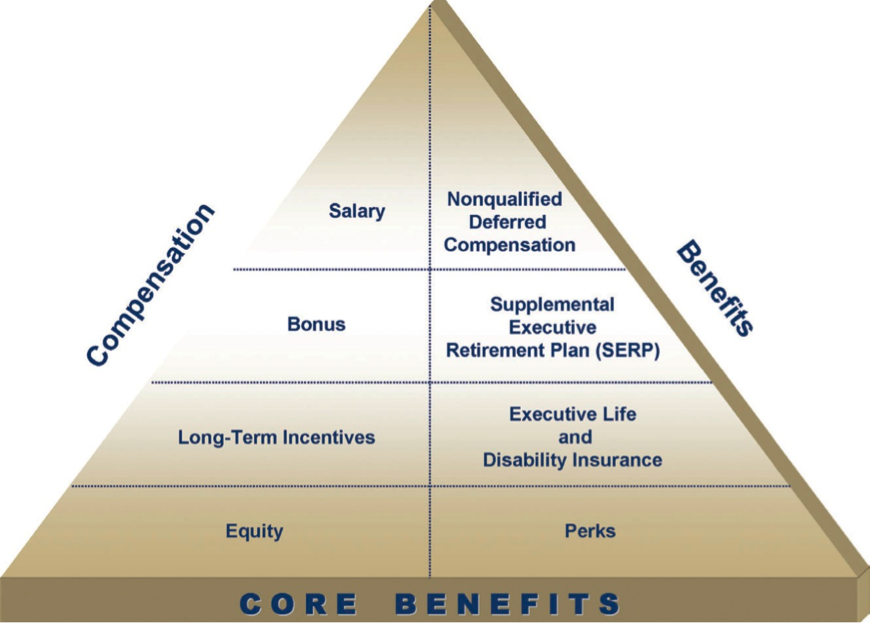

The Philosophy of Executive Compensation

When people review executive compensation they usually only discuss half the story. They tend to focus on the cash and equity side of the triangle and forget about executive benefits when, in fact, these benefits should fit into a company’s integrated total rewards program. In our last communication, we discussed the value of cash value life insurance. But did you know that the Life Income Strategy ™ can be used as:

- an incentive compensation program

- a funding vehicle for executive life programs

- an after-tax, tax-free retirement income plan

- an alternative to deferred compensation providing corporate tax deduction with no Sec. 409A compliance

“Executive benefits help to balance the overall savings and retirement strategy.”

MAF Companies works in concert with leading executive compensation consultants to help develop a “total compensation and benefits” strategy. Our job is to pro-actively control the experience of your clients, making their future more predictable.

Learn about The Life Income Strategy

Using a life insurance policy to help fund retirement? Did you know there is a strategy that will lend your client money for college expenses, a wedding, a vacation or even income taxes while all your

online slots premium dollars are at work building cash inside your policy?

Join John Ruggiero, MAF Chief Marketing Officer, for our first Tuesday Topic webinar as he discusses the Life Income Strategy:

Date: Tuesday, February 14th

Time: 10:00 a.m.-11 a.m CST

Meeting Number: 715 177 238

Meeting Password: Lifeincome123

To join this meeting:

1. Go to https://aimcor.webex.com/aimcor/j.php?J=715177238amp;PW=NY2NmZGQ2ZWFl

2. If requested, enter your name and email address.

3. If a password is required, enter the meeting password: Lifeincome123

4. Click “Join”.

5. Follow the instructions that appear on your screen.

Audio conference information:

To receive a call back, provide your phone number when you join the meeting, or call the number below and enter the access code.

1. Call-in toll-free number (US/Canada): 1-877-668-4490

2. Call-in toll number (US/Canada): 1-408-792-6300

3. Global call-in numbers: https://aimcor.webex.com/aimcor/globalcallin.php?serviceType=MCamp;ED=169932707amp;tollFree=1

4. Toll-free dialing restrictions: http://www.webex.co

m/pdf/tollfree_restrictions.pdf

5. Access code:715 177 238

The EPOCH Story

Word is getting around throughout the charitable giving community that a new endowment campaign financing facility is making possible $billions of donations to top charities, hospitals, and fraternal organizations.

The program I’m describing was created by a team of ex-Lehman Brothers and Bank of America Securities ABS professionals, and is being sponsored by some of the largest charitable endowments in the country.

Each program is run as a fund-raising campaign by the Non-Profit Organization (NPO) but is totally distinctive in that the donors as part of the EPOCH Program, receive premium loans for their entire lifespan on a non-recourse basis. Each donor agrees to have a $2.5 million universal life policy placed on his or her life, with the entire proceeds irrevocably dedicated to a trust whose beneficiary is the charity or qualifying NPO. Each tranche contains at least 400 donors-trusts for a total of $1 Billion in life insurance proceeds.

Life insurance trusts in themselves are not earth-shaking as they have been a standard planned-giving staple for years.

However, to further what I mentioned above, the premiums are paid by a master trust which is funded by an unusual form of security – the Life Insurance Financing Trust Security or “LIFTs”. The LIFTs are “loans for life,” which are collateralized by Irrevocable Life Insurance Trusts (ILITs) and, as an actuarially significant portfolio, are sold to major pension funds or to existing major charitable endowments in securitized form as LIFTs securities.

LIFTs securities are popular because they are high yield (10.5% IRR), non-correlating to the capital markets, liquid via rule 144 eligibility, and best of all, long duration (27 years). The buyers are also motivated by the duration-matching character of the collateral – all policies statistically “mature” by age 100 and are actuarially curved by the consulting actuaries to insure that significant annual payouts will occur throughout the 27 year life of the LIFTs security.

The LIFTs are designed to be issued via prospectus only from top securities broker-dealers.

I was amazed and full of questions when I reviewed the due diligence package on LIFTs and I’m sure most of you will be skeptical as well. But after considerable review, I am convinced that LIFTs make good sense and moreover, may be the answer to many of the problems faced today by both charitable fundraisers and by the defined benefit pension community.

If any of you in my blogosphere are curious about LIFTs and want more information, please contact me at (630) 834-2210 Ext 240. I’ll walk you through how it works in detail.

Selling in Today’s B2B Marketplace

I come from the old school of selling; cold calls to set appointments. The more calls you made, the more appointments you set and, in the end, the more sales you closed.

It’s not that simple anymore. The people you are trying to reach today just don’t answer the phone like they did in the old days. Today’s first meetings require a lot of leg work; networking, referrals, LinkedIn, etc. You have to work a lot harder today to “crack the door.”

So what happens in that first meeting today is especially critical to your success. I was trained in Solution Selling. Solution Selling’s premise is to ask the right discovery questions to uncover the prospect’s needs, or “pain points,” and let the prospect navigate to the conclusion that your product or service is the solution to solving the problem. As the sales professional, you are the problem solver for the prospective buyer.

In the current issue of Harvard Business Review, the claim is made that Solution Selling is dead, and today’s top sales professionals are using a new sales approach called read more

Insight Selling; a radically different approach to selling in a B2B environment. I’m not sold on the total premise of Insight Selling, but I strongly believe there are elements that can be used to improve your sales effectiveness with prospects.

One sales strategy with Insight Selling that applies to selling one of our strategies, 401k SAFE, is the idea of showing a prospect a solution that solves a problem that the prospect hadn’t previously identified. Outsourcing administrative functions, such as payroll, is not a new concept to employers, but outsourcing their 401(k) plan is a new concept for most employers, and an opportunity to educate, or provide insight to a prospect on how outsourcing the fiduciary, compliance and administrative burden can free up valuable resources and mitigate the risk associated with a non-profit generating function in their business. It’s a different approach to discussing traditional fund performance, plan services, and cost.

If you have a specific situation or would like to review how Insight Selling can change your prospecting methods, please call me at (800) 979-9393 or john@mafcompanies.com

Term Insurance: The Life Insurance Industry’s Stepchild

Term insurance is one of the most valuable life insurance products in the market. As you know, it provides life insurance for a “term” of time. In today’s marketplace, it has evolved from an annual increasing premium concept to a level premium structure offering level premiums for 10, 15, 20 or even 30 years.

There are riders that can be attached to the policy giving the contract more value-added features. If a client should face a disability, adding disability waiver of premium can be included and the insurance carrier will pay the life premium. Return of premium can be included by a rider or even issued as a stand-alone policy. Here the carrier will charge the extra premium so at the end of the term, all the payments are refunded. Child riders can be a good addition to the policy and protects the insurability of the children in the family…giving them a start.

The risk of term insurance is when the level premium comes to an end but the need continues; can the insured medically qualify for a new plan? Finding a term product with good conversion privileges is important. Term insurance pricing increases significantly if one’s health moves from the preferred health class to a standard or substandard class.

What I have discovered is how many advisors and clients do not realize that the term insurance market continues to be very competitive and a simple evaluation may produce significant savings. As I have preached in the past, life insurance is generally not managed or overseen properly.

Here are some recent case discoveries:

- A 40 year old male had a $1.5 million term policy with an increasing term premium structure. He wanted to be covered another 20 years. A new 20 year level term program saved him 30% over the 20 years. He pays more currently but over the 20 year period will save significantly over the increasing premium plan.

- A 50 year old bought a $2 million, 15 year level term plan 10 years ago. He could replace it with a new 10 year, level term plan for the same premium and the new plan gives him an extra 5 years of coverage.

- A business owner had $20 million of term that was issued with a table rating. We were successful in reducing the table rating to a standard risk saving about $10,000 per year.

- A client had $10 million of 20 year coverage that he bought 15 years ago. His need for life insurance has decreased based on a collaborative discussion with his other advisors and we reduced the coverage to $7 million for 10 years at the same premium, adding 5 more years to his program.

- A client was spending $30,000 for two whole life policies totaling $5.2 million. After an exhaustive and as he put it, “mind-numbing” analysis, we finally came to the conclusion that his true need was $20 million. He implemented a 20 year term plan…waiting to see how the tax laws and his needs unfold over the next 10 years.

Term insurance needs attention, too! It does not always save money but each case involved the critical thinking needed to make the necessary adjustments in their planning and need for life insurance.

We are here to help. Please call us at (800) 979-9393 for your case design needs.